If you’ve been relying on the “no asset limit” rules from a couple of years ago, it’s time for a quick refresher. As of January 1, 2026, California has officially reinstated the asset test for seniors and people with disabilities.

While the program remains a vital lifeline for long-term care, the “rules of the road” have changed. Here is what you need to know to navigate Medi-Cal in 2026.

What is Medi-Cal?

Medi-Cal is California’s version of Medicaid. It provides health coverage for individuals with limited income and resources. For many seniors, it is the only way to pay for the expensive skilled nursing home care that Medicare typically doesn't cover long-term.

Who Qualifies for Medi-Cal in 2026?

To qualify, you must meet both medical and financial requirements. The biggest change this year involves what you own.

The New 2026 Asset Limits

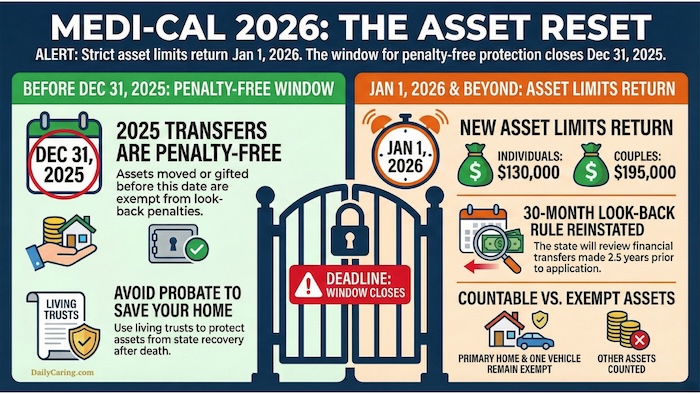

While California briefly removed the asset test for Medi-Cal, the rules shifted again on January 1, 2026. If you are applying for “Non-MAGI” Medi-Cal (the type most seniors use for long-term care), the state is once again looking at your bank accounts and investments. However, the 2026 limits are significantly more generous than the old $2,000 limit.

Use the table below to see where your household stands under the new requirements:

2026 Medi-Cal Asset Checklist: What Counts?

Before you submit your application, you’ll need to categorize your family's holdings. Under the new 2026 rules, Medi-Cal looks at “Countable Assets” to see if you fall under the $130,000 threshold. However, many of your most valuable possessions, such as your home, are considered “Exempt” and won't affect your eligibility.

Use this checklist to begin organizing your financial documents for the 2026 asset test:

The Medi-Cal Look-Back Period: Timing Your Planning

In California, the look-back period is 30 months (2.5 years). If you transfer assets for less than they are worth within that window, you could face a “transfer penalty” – a period where Medi-Cal refuses to pay for nursing home care, leaving you to foot the bill out of pocket.

However, there is a silver lining for those who acted early. Use this guide to see if your past or future gifts are “safe.”

Why This Matters for Your Application

The reinstatement of the 30-month look-back means “Notice of Action” letters will become much more common. If you are currently helping a loved one with their annual renewal, be prepared for the state to request bank records dating back to 2023 or 2024 to verify your claims.

If you're feeling overwhelmed by the paperwork, it’s worth checking out our guide on how to stay organized during a health crisis to keep your documents and your sanity in check.

Estate Recovery: Is Your Home Safe?

Many families worry that the state will “take the house” after a loved one passes away. In California, Estate Recovery is limited to assets that pass through probate.

This means that if you use a living trust or joint tenancy to pass your home to heirs outside of probate, the state generally cannot claim it. According to the California Advocates for Nursing Home Reform (CANHR), proactive planning is the best way to protect an inheritance while still accessing the benefits your loved one deserves.

Medi-Cal Application Tips for 2026

- When to Apply: You can apply at any time through Covered California. There is no specific window for Medi-Cal.

- Medicare Alignment: If you already have Medicare, Medi-Cal can act as a secondary payer. Ensure you maximize your Medicare coverage so that the two programs work in tandem.

- Documentation: Be prepared to provide bank statements and property records. The state will now scrutinize these to ensure you meet the $130,000 threshold.

VIDEO: Medi-Cal Eligibility Updates for 2026

Next Steps: Your Medi-Cal Action Plan

Now that you have the 2026 roadmap, it’s time to put it into motion. Don’t wait for a renewal notice to arrive before you start organizing. Use these resources to take the next step in securing your loved one’s care:

- Clear the Confusion: Read our breakdown of the 5 Medicaid Misconceptions Caregivers Need to Know About to ensure you aren't falling for common myths that could cost you thousands.

- Strategic Spending: If your assets are slightly over the $130,000 limit, learn how a Medicaid spend-down works in 2026 to legally qualify without “giving away” the family legacy.

- Get Expert Eyes: For free, one-on-one help with your specific situation, find your local State Health Insurance Assistance Program (SHIP) counselor. They are experts in navigating the intersection of Medicare and Medi-Cal.

- Launch Your Application: When you’re ready to apply or manage an existing case, use the official BenefitsCal portal—the fastest way to submit documents directly to your county.

Your 3-Step 2026 Action Plan

“Navigating Medi-Cal is a marathon, not a sprint. Take the first step today.”

Summary: Medi-Cal 2026

The 2026 changes mean that “winging it” is no longer an option for California caregivers. With the asset test back in play, staying informed and keeping your assets positioned correctly is the only way to ensure care isn't interrupted.

For more help with your family's finances, see our guide on how caregivers protect their financial health while managing these complex programs.

Legal & Financial Notice:

The 2026 Medi-Cal rules are complex and subject to specific county interpretations. This guide is for informational purposes and does not constitute legal or financial advice. We strongly recommend visiting the California Department of Health Care Services (DHCS) or consulting an elder law attorney to discuss your specific situation.

About the Author

Chris is a seasoned healthcare executive and entrepreneur from the Pacific Northwest. He strongly advocates for older adults and the caregivers who serve them. Chris has personal experience caring for his father, who had dementia. Chris is a technology enthusiast and an avid outdoorsman; if he's not in his office, he can usually be found on a golf course or fly-fishing out west somewhere.